The power of affordable credit sets out the case clearly. More than 20 million people in the UK live in financially vulnerable circumstances. The unmet demand for responsible credit is around £2bn a year. Better access to small-sum lending could add £5.9bn to £6.4bn to the UK economy each year.

The article also makes an admission that most of the sector still avoids saying out loud:

"the current speed of growth of affordable credit isn't close to meeting the challenge facing millions of people across the country. Simply put, we need to try a new approach."

That sentence is the most important one in the piece. It is also the one the rest of the article does not really answer.

The "new approach" Fair4All goes on to describe — more capital, more subsidy, more bank-to-CDFI referrals, more guarantees, more first-loss funding — is, with respect, not a new approach. It is a larger, better-funded version of the existing one.

The £40m committed through the Scale Up Programme is real money. The 238,000 loans worth £161m delivered by investees in 2025 are real loans to real people. But against a £2bn annual unmet need, £161m of new lending is roughly eight pence on the pound. That gap is not closing on this trajectory. It is widening every quarter we choose to be patient.

The country does not have time for incremental.

The unit economics problem

A £500 loan to a customer with a thin file, irregular income and a need for wraparound support costs a community lender almost the same to originate, decide, service and collect as a £50,000 loan costs a bank to lend to a prime customer.

The credit risk is different. The regulation is different. The affordability work is harder. But the operational cost — manual review, manual outreach, manual collections — is broadly fixed.

That is why mainstream lenders walked away from small-sum lending in the first place. It is also why credit unions and CDFIs, even when they are well run and well capitalised, struggle to push past a few thousand active borrowers without their cost base eating their margin.

Capital does not fix this. More capital into a model where every additional loan costs roughly the same to serve as the last one just pushes break-even further out.

Subsidy does not fix it either. Subsidy keeps the existing model alive. It is not a route to a model that works on its own terms.

Guarantees and first-loss funding shift risk. They do nothing for cost-to-serve.

As long as a small-sum, vulnerable-borrower loan needs a human in every loop, this sector will be permanently dependent on the patience of social investors and the political appetite for transfers from elsewhere. That is not scale. That is life support.

What "tech transformation" has actually meant

Fair4All notes that part of its £40m has gone into "technology transformations" at investee organisations. We see the output of that work every week.

In most cases, what it has produced is a digitised version of the paper-and-spreadsheet model that came before. Online application forms feeding manual underwriting queues. Customer portals bolted on to legacy core systems. Slightly faster decisions made by slightly more efficient humans.

That is not transformation. That is the same operating model behind a nicer screen.

The reason the curve is not bending fast enough is that we have been investing in tools that make the existing process run a little faster — when what the sector needs is a process that does not depend on the existing labour at all.

Fund the digitisation of a manual model and call it transformation, and we end up writing the same article in 2027. Slightly bigger gap. Slightly more urgent language. Same problem.

A challenge to credit unions: the numbers tell their own story

This part of the conversation is rarely had in public. It should be.

We pulled the published accounts of 43 UK credit unions covering 2019 to 2024 — broadly the cohort that sits at the heart of Fair4All's Scale Up Programme — and looked at what the financial statements actually say about how this sector uses the capital it already has.

The headline finding is uncomfortable.

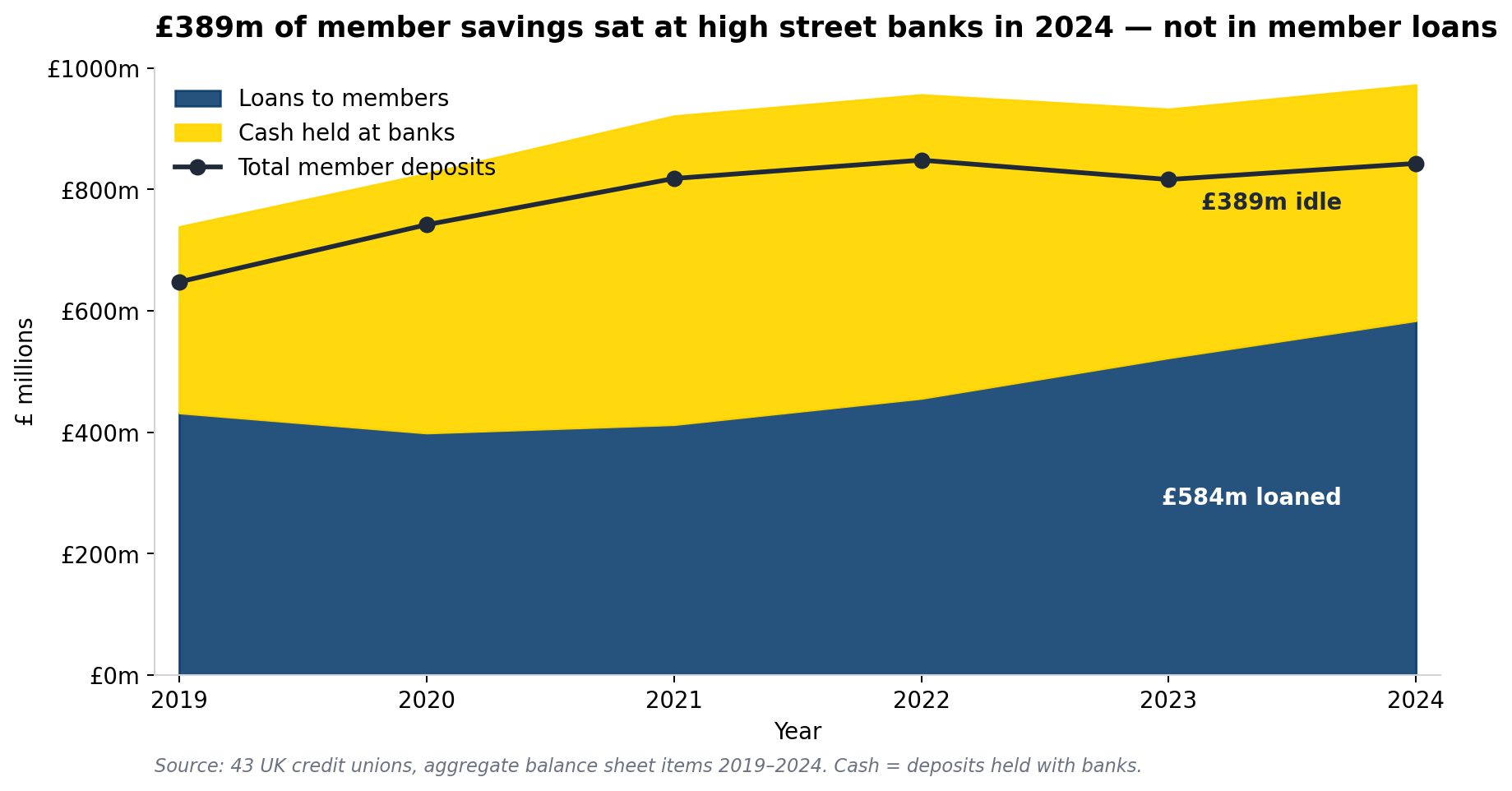

At the latest filed year, members had entrusted these 43 credit unions with £843m of deposits. Only £584m was lent to other members. The remaining £389m was sitting in deposits at high street banks.

Forty-six pence in every pound members saved with their credit union was not reaching another member as a loan. It was earning a clearing-bank rate, while Fair4All's research describes a £2bn unmet credit gap and millions of people turning, in extremis, to illegal lenders.

The trend is no comfort either.

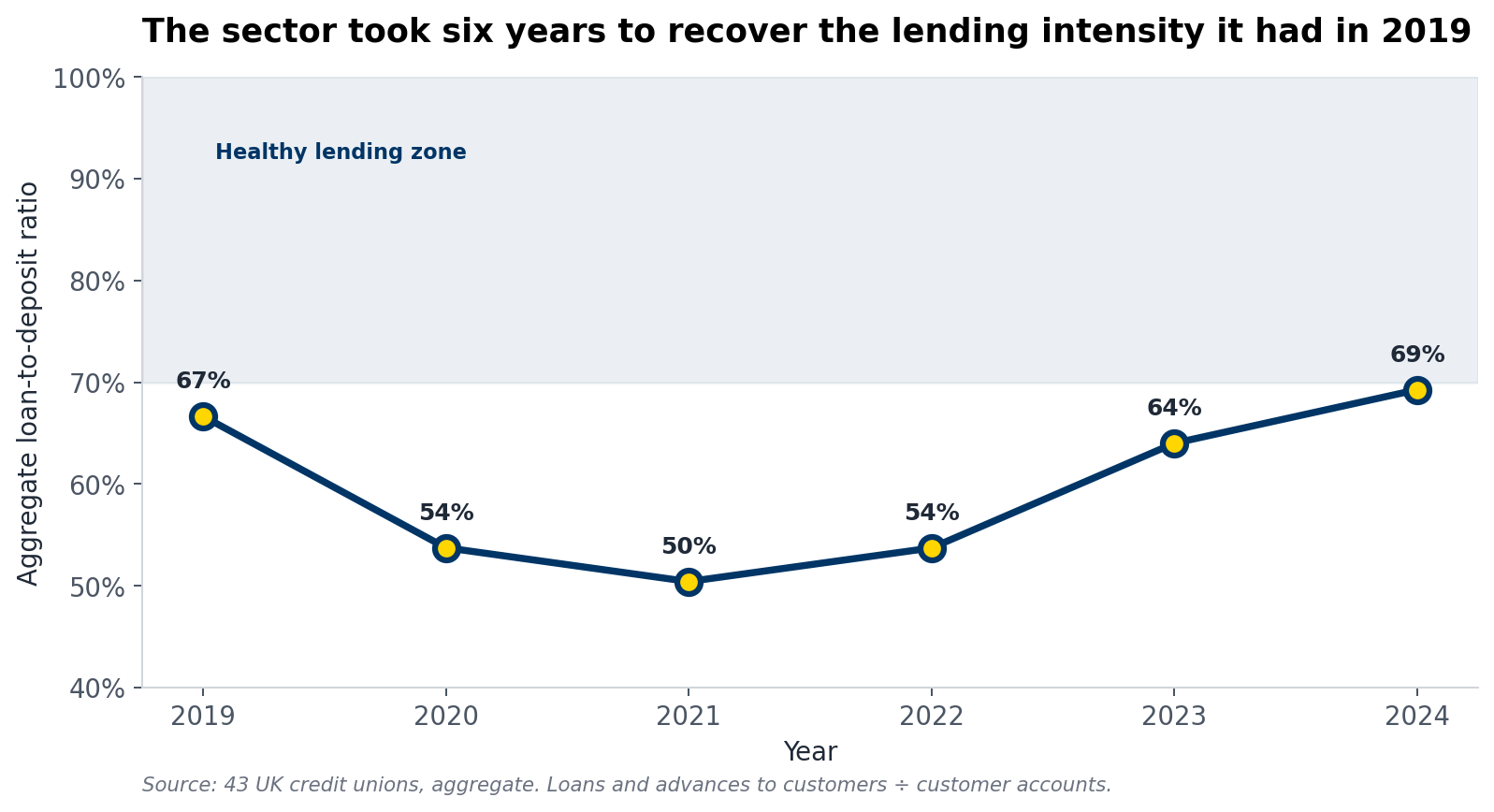

In 2019, the aggregate loan-to-deposit ratio across this cohort was 67%. By 2021 it had fallen to 50%. As of the latest year it has clawed its way back to 69%.

The sector took six years just to recover the lending intensity it already had before the pandemic — across the same six years in which the underlying need rose, not fell. There is no plausible reading of those numbers in which the binding constraint is a shortage of deposits.

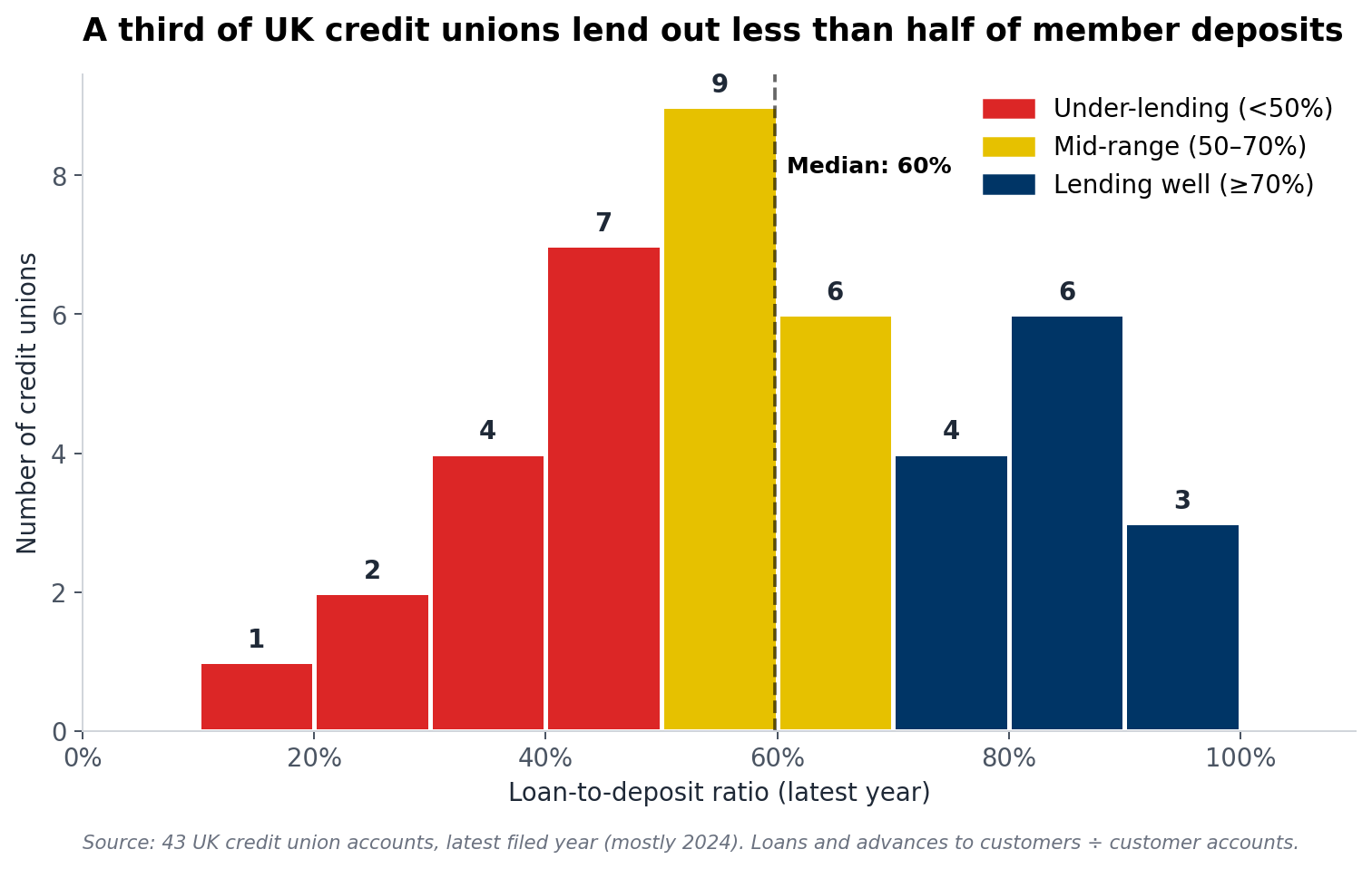

Inside the cohort, the picture is sharper still.

A third of the credit unions in the dataset — 14 of 43 — were lending out less than half of the money their members had saved with them. Three were below 30%. The median credit union has a loan-to-deposit ratio of 60%.

These are not radical critiques. They are descriptive statistics from the institutions' own filings.

The natural defence is prudential. Small lenders need a liquidity buffer. Members need to be able to withdraw. The regulator expects a margin of safety. All true. None of it explains a sector-wide cash buffer of 46% of deposits.

Even on a deliberately conservative reading — a 20% liquidity floor across the board, well above what any solvent credit union actually needs day to day — there is around £90m of additional lending capacity sitting unused inside this cohort alone.

That number rivals the entire £40m Fair4All has so far committed through the Scale Up Programme. The sector is sitting on more dry powder than its primary social investor has put on the table — and it is not deploying it.

The reason it is not deploying it is the same reason the Fair4All model is the size it is. The unit economics do not work.

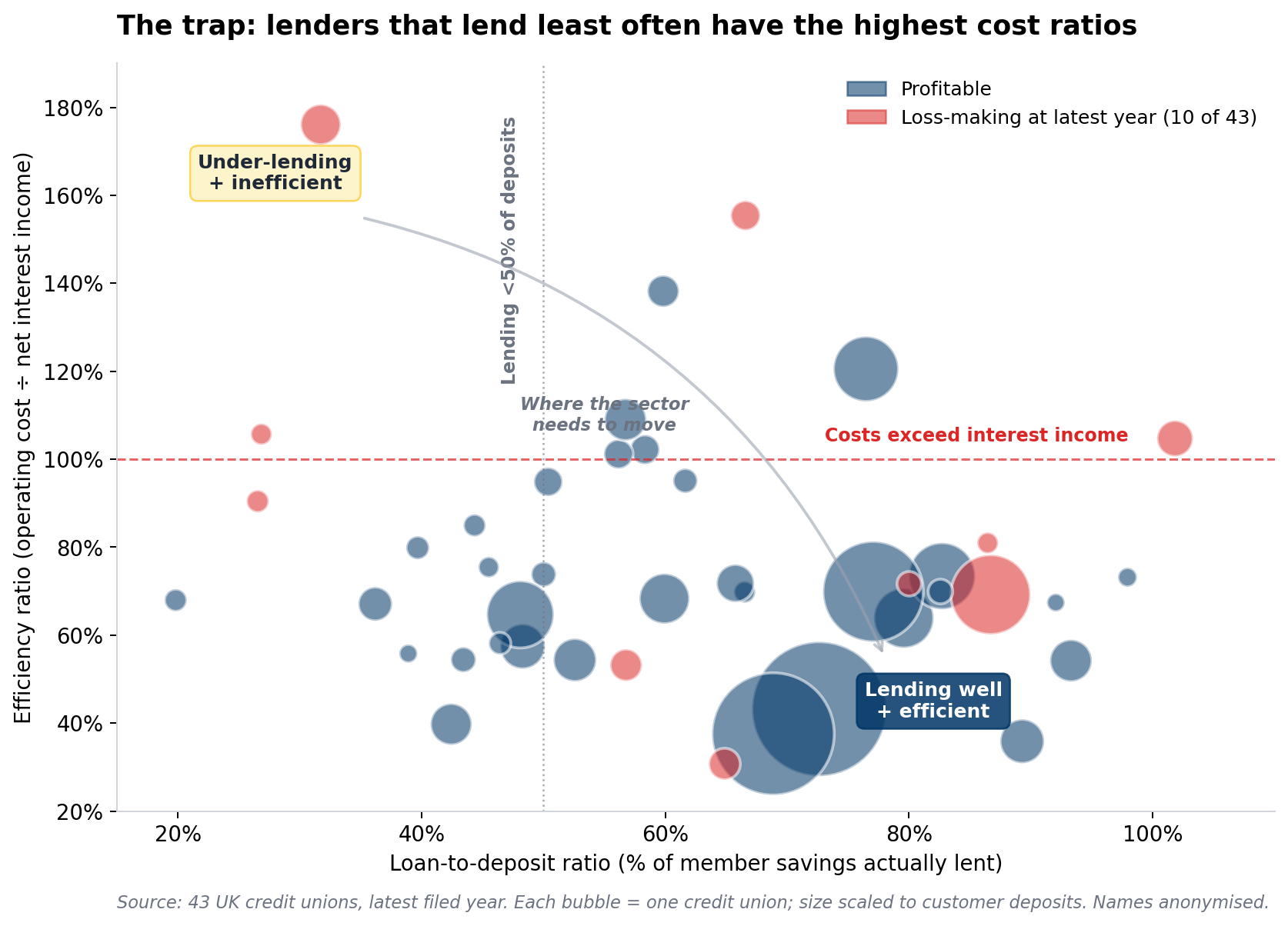

Look at the cost side and the picture sharpens immediately. The median efficiency ratio across these 43 credit unions is 70%. Every pound of net interest income costs 70 pence to generate. The mean is 78%.

Nine of 43 — more than one in five — have an efficiency ratio above 100%. Their core lending operation loses money on operating cost alone, before a single bad debt is provisioned.

Ten of 43 are loss-making at the latest year.

And the credit unions that lend the least often have the highest cost ratios of all. That is not a coincidence. It is the logic of a fixed-cost manual operation running at sub-scale.

So the challenge to the credit union sector is this.

The capital is in the building. Members have already entrusted you with it.

The barrier to lending it out responsibly to the people Fair4All Finance has spent ten years arguing should have access to it is not deposits. And it is not, increasingly, social investment.

It is the cost-to-serve of your existing operating model — and the way that cost forces a defensive posture toward your own balance sheet.

Asking members to keep saving with you while half of those savings sit at NatWest is not a sustainable answer to the question Fair4All has put to the sector.

This is not a criticism of credit union boards or executives, who are running the model they inherited as well as it can be run. It is an argument about what the next investment cycle has to be for.

Funding another iteration of the same model — a slightly slicker portal, a slightly faster decision engine bolted on to the same manual back office — will not move these numbers. It will give us the same chart in 2027.

What it actually takes to scale

This is where the conversation has to change. And it is where Credit Canary exists.

The path to scaling affordable credit at the speed Fair4All's own numbers demand runs through end-to-end agentic automation of the lending lifecycle: origination, underwriting, decisioning, payment, engagement, and the strategy layer that sits above them.

Not chatbots bolted on to call centres. Not credit models that hand off to a human at the moment of decision. Specialist AI agents that own complete operational stages, with clear governance, full auditability, human oversight where it genuinely matters, and unit costs that fall an order of magnitude rather than a few percentage points.

When that shift happens, the arithmetic inverts.

A community lender with a small ops team can run the active book of a much larger one. The cost-to-serve on a £500 thin-file loan begins to approach the cost-to-serve on a £5,000 mainstream one.

The £389m of idle cash in the cohort above stops being a prudential necessity dictated by operational cost. It starts being lendable capital.

Efficiency ratios over 100% become an artefact of the past, not a structural feature of inclusive lending.

Fair4All's £40m, instead of being the ceiling of what this sector can absorb, becomes the seed capital for a model that can finally compound.

This is not a future-state thesis. It is the work we are doing now, with community lenders and non-bank commercial lenders who have already accepted that capital and goodwill alone will not get them where they need to be.

A direct call to Fair4All Finance: deploy faster, deploy bigger

We want to be unambiguous about what we are arguing here.

Fair4All Finance is the right body, in the right position, with the right mandate to lead the closing of the affordable credit gap. There is no other organisation in the UK landscape with the same combination of capital, convening power, sector legitimacy and political reach.

The criticism that gets levelled at Fair4All from time to time — that it is not the answer to every question in inclusive finance — misses the point. It is the most important answer we have to this question, and it should be backed accordingly.

Which is exactly why the speed of deployment matters so much.

The £40m committed through the Scale Up Programme is meaningful. It is also being released into the market on a cadence that is calibrated to the operational absorption capacity of the existing model.

That is rational on its own terms — there is no point shovelling capital into investees who cannot deploy it responsibly. But it is also the binding constraint dressed up as prudence.

The pace of capital out of Fair4All today is fundamentally limited by the pace at which the sector can operationally process more lending. The data above says the same constraint is what keeps £389m of member savings parked at the high street rather than reaching borrowers.

Break that operational ceiling, and the case for moving the capital faster, in larger tranches, with bolder matched commitments from commercial partners, becomes overwhelming.

So the championing call is this. Fair4All Finance should be deploying meaningfully more capital, into the market, faster — and the public conversation should be pushing them to, not asking them to be patient.

The 20 million people the article opens with are not in a position to wait for a five-year capital roll-out. The 4% of the population using illegal lenders are not waiting either.

The demand is now. The capital is there. The political case is made. The remaining bottleneck is operational — and that bottleneck is fixable in 2026, not 2030, with the technology that already exists.

The pairing has to be explicit:

- Faster, larger capital deployment from Fair4All into the affordable credit ecosystem.

- Matched with investment in the kind of operating model that can absorb that capital responsibly and turn it into ten times the lending volume per pound the sector achieves today.

Capital alone will not close the gap. Automation alone will not close the gap. The two together, deployed at the cadence the demand actually requires, will.

A challenge, respectfully offered

The challenge for Fair4All Finance, for the credit union sector, and for the wider community of investors, regulators and policymakers is this.

Capital is necessary. Without it, none of this happens.

Capital is not sufficient.

Without a parallel, deliberate, urgent investment in the operating model — specifically, in agentic automation that collapses the cost-to-serve of small-sum, vulnerable-borrower lending — the next report on the state of affordable credit, written in 2027 or 2028, will read remarkably like this one.

The numbers will be slightly larger. The gap will be slightly wider. The "new approach" will still be needed. The illegal lenders will still be there. The £389m will still be sitting at the bank.

We agree with Fair4All Finance that affordable credit can transform individual lives and add billions to the UK economy. We agree that the current speed of growth is not enough.

Where we would push the conversation further is on the how and the when.

The how, in 2026, is end-to-end automation. The when is now. Not as a side investment. As the strategy.

The £2bn gap will not be closed by lending more carefully through the same model. It will be closed by lenders who can finally afford to say yes — and by an investor of last resort who is willing to deploy capital at the cadence the country actually needs.

Note on the data: aggregate balance-sheet figures cited above are drawn from the published accounts of 43 UK credit unions covering 2019–2024. The dataset, our calculations and the supporting charts are available on request.

← Back to News & Opinion